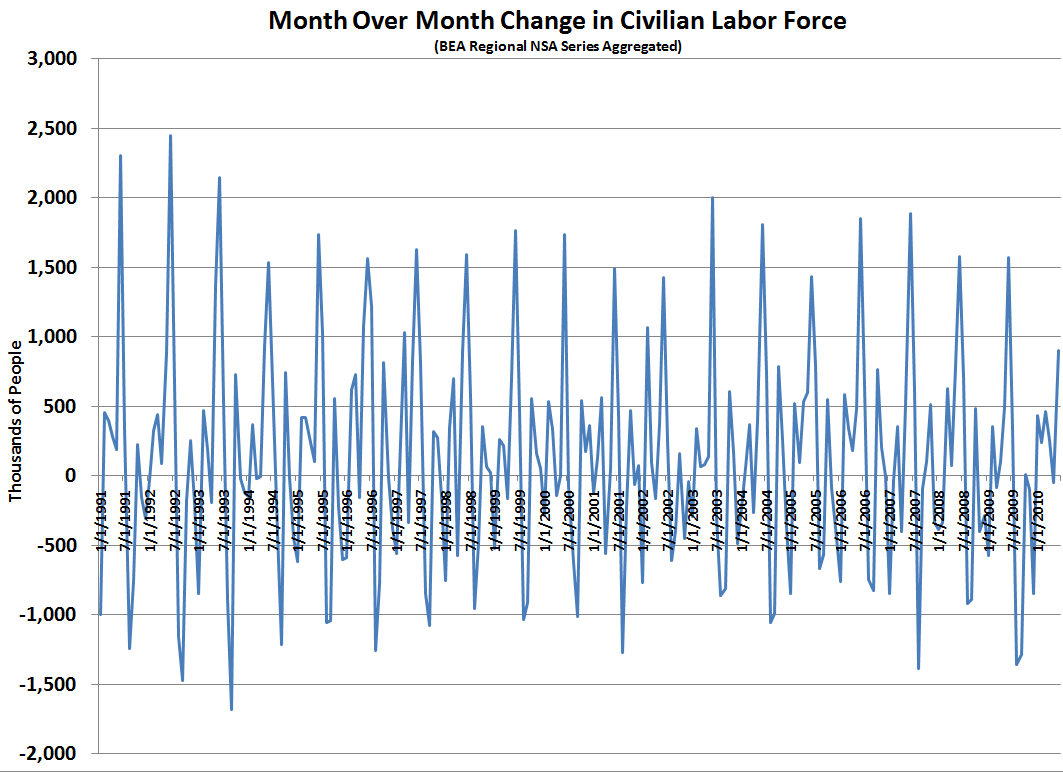

So here is the labor force, in thousands of persons pulled from the St. Louis Fed FRED database by aggregating the eight regional data sets (non-seasonally adjusted). It pretty much grinds upwards at the rate of population growth, with some seasonality around the trend line...until recently.

As a fan of non-seasonally adjusted (NSA) data, one way to account for seasonal effects is to look at the data on a year over year basis, which we see above. The data series is right at twenty years, so it is not that long...but we see one striking observation with respect to changes in the size of the labor force on a year over year basis, there aren't any negative values until recently.

Now I have a quirk about trying to quantify things, but a meaningful framework of analysis is often the tricky bit (which is not to say that I have cracked that nut here!).

So, the approach I took was to compare the values for year over year change for the month of June across the data set, a total of twenty observations. I took the first nineteen to be from the same distribution, and assumed a normal distribution (quite arguable, but it keeps the spreadsheet work simple). Using the mean and standard deviation derived, if the last observation is from the same distribution, where does it fit?

For the June, 2010 year over year change in the labor force, the value is 4.5 standard deviations out which is, umm improbable...suggesting that this observation is from a different distribution, which I interpret as an indication of structural changes in the make up of the US labor force.

Examing the month over month change for the time series, a strong seasonality is clearly indicated. A comparison of June values only but for month over month changes might also be indicative...

So what does the month over month change tell us for June, 2010? Now we are only 3 standard deviations out, which is still <1%...

So, this would appear to be an armchair indication of structural changes in the labor force and hence reflected in the labor force participation rate, EMRATIO and the like.